Are individual retirement accounts taxable?

Traditional IRAs Amounts in your traditional IRA, including earnings, generally aren’t taxed until distributed to you. IRAs can’t be owned jointly.

Does opening an IRA help with taxes?

Traditional IRA Contributions Are Deductible A traditional IRA is funded using pre-tax dollars. That means that once you start taking distributions, you’ll have to pay taxes on the money at your regular rate. The upside is that you can deduct the money you put in, which can reduce your taxable income for the year.

How much will IRA reduce taxes?

Traditional IRA contributions can save you a decent amount of money on your taxes. If you’re in the 32% income tax bracket, for instance, a $6,000 contribution to an IRA would shave $1,920 off your tax bill.

How much money can you make in retirement without paying taxes?

If you’re 65 and older and filing singly, you can earn up to $11,950 in work-related wages before filing. For married couples filing jointly, the earned income limit is $23,300 if both are over 65 or older and $22,050 if only one of you has reached the age of 65.

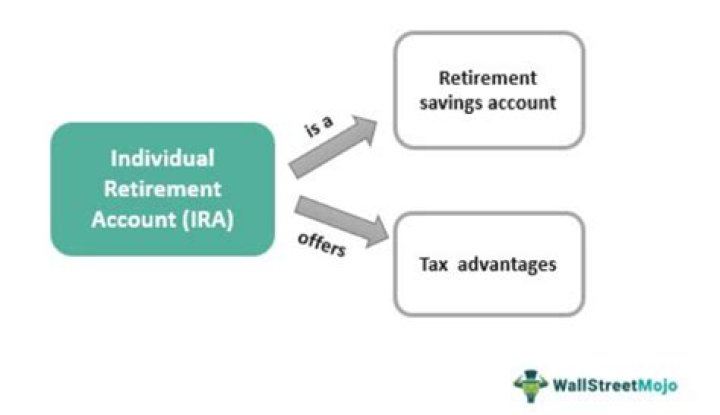

What kind of account is an Individual Retirement Account?

What Is an Individual Retirement Account (IRA)? An individual retirement account (IRA) is a tax-advantaged investing tool that individuals use to earmark funds for retirement savings. There are several types of IRAs. Traditional IRAs.

Can you contribute to an Individual Retirement Account ( IRA )?

Choices include banks, brokerage companies, federally insured credit unions, and savings and loan associations. Most individual investors open IRAs with brokers. Note that you can only contribute to an IRA with earned income that meets IRA rules. Income from investments, Social Security benefits, or child support does not count as earned income.

What’s the exemption for an Individual Retirement Account?

Bankruptcy status. The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 expanded the protection for IRAs. Certain IRAs (rollovers from SEP or Simple IRAs, Roth IRAs, individual IRAs) are exempt up to at least $1,000,000 (adjusted periodically for inflation) without having to show necessity for retirement.

When did the Individual Retirement Account become legal?

Individual retirement arrangements were introduced in 1974 with the enactment of the Employee Retirement Income Security Act (ERISA). Taxpayers could contribute up to fifteen percent of their annual income or $1,500, whichever is less, each year and reduce their taxable income by the amount of their contributions.