Are IRA contributions based on tax year?

To be counted as a contribution for the prior year, you have to place your money in the account by the tax filing deadline for that year. For example, if you have a traditional IRA, you have from January 1, 2021, to April 15, 2022, to place money in your IRA and count those contributions on your 2021 tax return.

Can I still contribute to an IRA for tax year 2020?

This year, your federal taxes are due May 17, which might spark some confusion for retirement savers wondering if they can still make 2020 contributions to their IRAs through the new tax deadline. The answer is yes — you can make 2020 contributions to your IRA through May 17.

What is the maximum IRA contribution for 2019 tax year?

$6,000

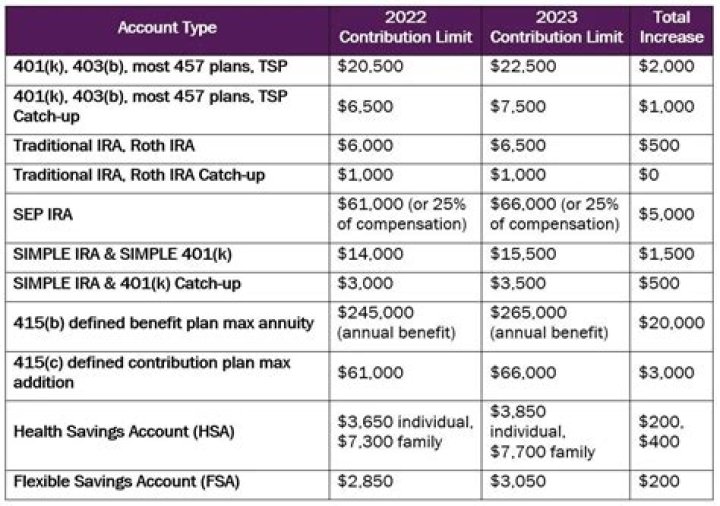

In addition, low and moderate-income taxpayers who make contributions to a traditional or Roth IRA may also qualify for the Saver’s Credit. Eligible taxpayers can usually contribute up to $6,000 to an IRA for 2019. The limit is increased to $7,000 for taxpayers who were age 50 or older by the end of 2019.

Can you contribute to previous year IRA?

You get three extra days to file your taxes. Fortunately, however, you can make prior year IRA contributions up until the tax filing date. So if you meant to start an IRA last year but forgot, you can still open an account, fund it, and count the contributions for the prior tax year.

Are there limits on how much you can contribute to a traditional IRA?

For 2018, 2017, 2016 and 2015, the total contributions you make each year to all of your traditional IRAs and Roth IRAs can’t be more than: The IRA contribution limit does not apply to: Your traditional IRA contributions may be tax-deductible.

How to document traditional IRA contributions for taxes?

Your IRA trustee mails you a Form 5498 every year you make a traditional IRA contribution. In the event of an audit, this form will suffice as evidence of your contributions. You do not need to include Form 5498 when you file your tax return.

Can a 70 year old contribute to a traditional IRA?

You can’t make regular contributions to a traditional IRA in the year you reach 70½ and older. However, you can still contribute to a Roth IRA and make rollover contributions to a Roth or traditional IRA regardless of your age.

When did the IRA contribution limit go up?

2001’s Economic Growth and Tax Relief Reconciliation Act increased contribution limits for 2002, and introduced ‘Catch Up’ contributions for 50 year old and older workers. EGTRRA also changed the contribution limits by statute, and indexed future increases in the contribution limit to inflation.