Can you carry over K-1 losses?

Partners and shareholders of S-Corporations are subject to three separate limitations on the losses and deductions reported to them on Schedule K-1 . Any amount of loss and deduction in excess of the adjusted basis at the end of the year is disallowed in the current year and carried forward indefinitely.

Can you carry forward Nonpassive losses?

Generally, losses from passive activities that exceed the income from passive activities are disallowed for the current year. You can carry forward disallowed passive losses to the next taxable year. A similar rule applies to credits from passive activities.

What happens to passive losses at death?

When a person with suspended passive losses dies, the losses may be claimed on the deceased’s final income tax return. Generally, for income tax purposes, the basis of an appreciated asset is stepped up to its fair market value as of the date of death.

How are k1 losses carried forward?

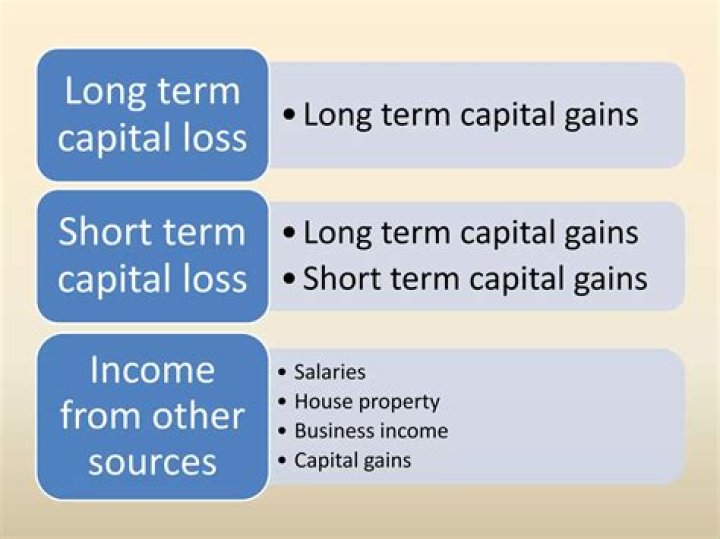

Your Schedule K-1 loss will first offset long-term capital gains from the same year. If the loss isn’t absorbed that way, it offsets short term capital gains. If a loss still remains, you can reduce future ordinary income by up to $3,000 per year on page one of Form 1040 until you use up all of the loss.

Do K-1 losses do tax treatment?

If your K-1 shows a net loss, you report it on the appropriate tax schedule, for example Schedule E for a partnership. Then you write in the loss on your Form 1040 and deduct it from any other taxable income. As long as you end up in the black overall, you can deduct all your losses.

Can corporations carry over losses?

At the federal level, businesses can carry forward their net operating losses indefinitely, but the deductions are limited to 80 percent of taxable income. Prior to the Tax Cuts and Jobs Act (TCJA) of 2017, businesses could carry losses forward for 20 years (without a deductibility limit).

Do I have to report k1 loss?

Yes, you should enter the K-1 on your tax return even if it shows a loss. It is a passive loss. The instructions mean that you are not allowed to deduct this loss from your other income. They are suspended to be used when you have a passive profit or when you sell the units.

Is K-1 income passive?

Line 1 – Ordinary Income/Loss from Trade or Business Activities – Ordinary business income (loss) reported in Box 1 of the K-1 is entered as either Non-Passive Income/Loss or as Passive Income/Loss.

Where do you report a loss on a K-1?

K-1 Losses. If your K-1 shows a net loss, you report it on the appropriate tax schedule, for example Schedule E for a partnership. Then you write in the loss on your Form 1040 and deduct it from any other taxable income.

How to carry over non passive loss from Schedule K-1?

TurboTax computes all of that for you. Any suspended losses are carried over to the next year. You can see those fields in Forms Mode. Open the K-1 and scroll down to Section A. Column (b) receives the transfer from your prior year return and the current year’s suspended amounts are in column (d).

What do you need to know about the K-1 form?

IRS Schedule K-1 is the schedule that partnerships, S corporations and limited liability companies use to report business income and losses. If, for example, you and two partners own the company equally, your individual K-1 forms will assign each of you one-third of the profits.

What are the basis limitations for Schedule K-1?

The basis limitation is a limitation on the amount of losses and deductions that a partner of a partnership or a shareholder of a S-Corporation can deduct. The basis limits are the first of three limitations that are applied to Schedule K-1 losses and deductions. After the basis limits are applied, the At-risk limits (Form 6198) are applied.