Can you give away life insurance proceeds?

If you want your life insurance proceeds to avoid federal taxation, you’ll need to transfer ownership of your policy to another person or entity. New owners must pay the premiums on the policy. However, you can gift up to $15,000 per person in 2020, so the recipient could use some of this gift to pay premiums.

How do transfer on death accounts work?

A transfer on death (TOD) account automatically transfers its assets to a named beneficiary when the holder dies For example, if you have a savings account with $100,000 in it and name your son as its beneficiary, that account would transfer to him upon your death.

Can death benefits be rolled over?

ERISA protects surviving spouses of deceased participants who had earned a vested pension benefit before their death. whether death benefit payments from the plan may be rolled over into another retirement plan; and. if a rollover is possible, the method and time period in which the rollover must be made.

If you want your life insurance proceeds to avoid federal taxation, you’ll need to transfer ownership of your policy to another person or entity. New owners must pay the premiums on the policy. However, you can gift up to $15,000 per person in 2020 and 2021, so the recipient could use some of this gift to pay premiums.

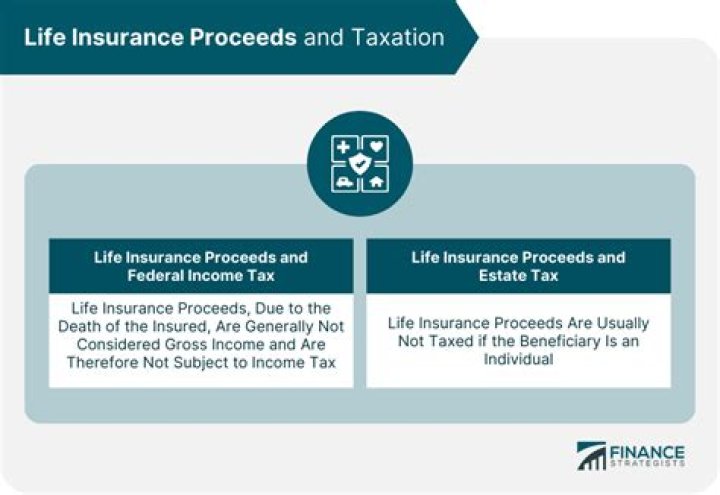

Are life insurance proceeds part of an estate?

Life insurance policies only become part of an estate if the policy owner directs the insurance company to pay the estate upon their death or if they neglect to name a beneficiary. If the estate is the beneficiary of the policy, most states require the insurance company to pay the probate court directly.

What happens to the proceeds of a life insurance policy?

Life insurance policy proceeds can be used to pay estate taxes When a person with a life insurance policy dies, there is a lot of confusion about the taxation of the proceeds. The tax consequences of being the beneficiary of a life insurance policy can be confusion, but this information should help.

How to avoid taxation on life insurance proceeds?

Taxation of Life Insurance Death Benefits. One of the benefits of owning life insurance is the ability to generate a large sum of money payable to your heirs in the event of your death. An even greater advantage is the federal income-tax free benefit that life insurance proceeds receive when they are paid to your beneficiary.

How can I remove life insurance proceeds from my estate?

A second way to remove life insurance proceeds from your taxable estate is to create an irrevocable life insurance trust (ILIT). To complete an ownership transfer, you cannot be the trustee of the trust and you may not retain any rights to revoke the trust.

When is life insurance included in an estate?

Inclusion in the estate can be avoided if the policy is owned by someone else, or by a trust Life insurance policy proceeds can be used to pay estate taxes When a person with a life insurance policy dies, there is a lot of confusion about the taxation of the proceeds.