Do closely held corporations pay dividends?

Furthermore, most closely-held corporations do not pay out dividends, or at least do so very, very rarely. The payment of corporate dividends results in a tax penalty. Corporate profits are taxed when received by the corporation, and are then taxed again when received by the shareholders.

Where should a corporation Record paying for cash dividends?

Cash dividends do not affect a company’s income statement. However, they shrink a company’s shareholders’ equity and cash balance by the same amount. Firms must report any cash dividend as payments in the financing activity section of their cash flow statement.

What happens when a company pays a cash dividend?

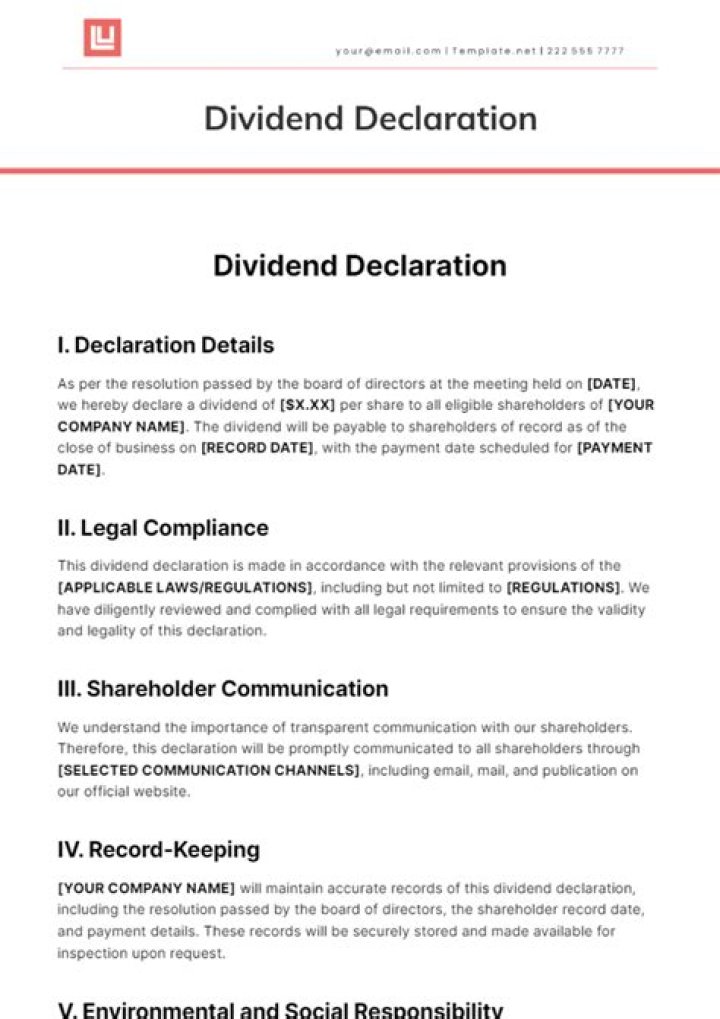

On the day a company declares to the public that it is paying its investors a dividend, the CEO or board of directors authorizes the amount of the dividends payable. The company then debits retained earnings and credits dividends payable for the total amount of authorized dividend payment amount.

What is the difference between a closely held corporation and a publicly held corporation?

The closely held corporation is often a private corporation, with restrictions on who can hold shares. A publicly held corporation typically has many shareholders; as a public company, they cannot restrict who can obtain shares, which are listed on public stock exchanges.

How are shareholders of a closely held corporation paid?

In a closely held corporation, two or three shareholders may agree to advance themselves an amount in proportion to their stock ownership rather than pay salaries or dividends.

Can a closely held corporation pay constructive dividends?

[iv] In the case of a closely held corporation, shareholders must also be attuned to the risk of constructive dividends distributions. [v] This is also key for the corporation, which will be treated as having sold the property distributed if the fair market value of the property exceeds its adjusted basis in the hands of the corporation.

How are corporate dividends taxed to a shareholder?

This means that the tax rate applicable to a redemption taxed as a nonliquidating corporate distribution (taxable dividend to the extent of the corporation’s E&P) may actually be 18.8% (15% + 3.8%) or 23.8% (20% + 3.8%). A cash distribution to a shareholder is a taxable dividend to the extent of the corporation’s current or accumulated E&P.

How are loans used to extract cash from closely held corporations?

Using Loans to Extract Cash From a Closely Held Corporation. Lending corporate cash to shareholders can be an effective way to give the shareholders use of the funds without the double-tax consequences of dividends. However, an advance or loan to a shareholder must be a bona fide loan to avoid a constructive dividend.