Do non profits file a 10k?

Form 990, like Form 10-K that private sector publicly traded firms file, is the key primary document for not-for-profit researchers.

Can you have a nonprofit in two states?

As mentioned in that article, it is possible to operate in multiple states. If an organization is planning to conduct any type of activity outside its incorporated state, certain measures need to be taken to maintain state-level compliance.

Are non profits required to publish salaries?

Answer. Indeed. Nonprofits are required to submit their financial statements and other information — including the salaries of directors, officers, and key employees — to the IRS. The IRS and nonprofits themselves are required to disclose the information on Form 990 to anyone who asks.

What kind of tax return do nonprofits have to file?

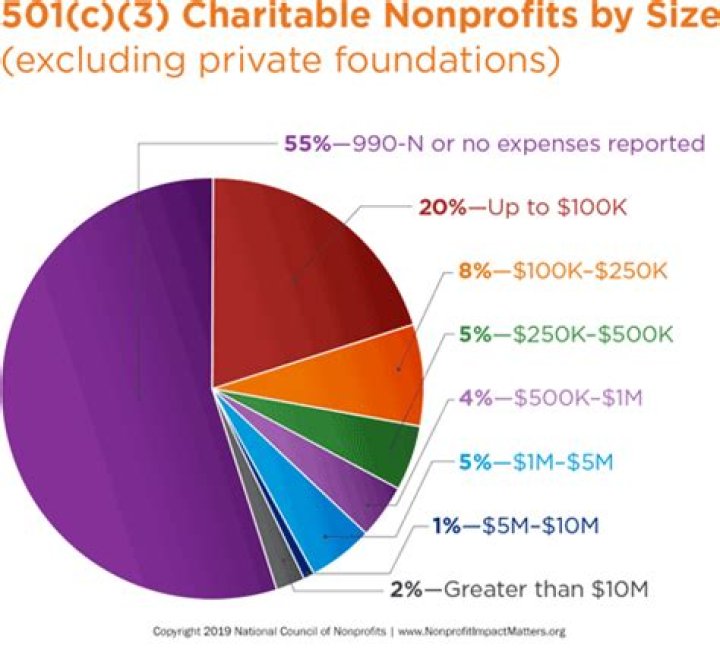

All private foundations file Form 990-PF. Tax-exempt organizations with gross receipts of $200,000 or assets worth $500,000 file the Form 990. Nonprofits with gross receipts of less than $200,000 but more than $50,000 file Form 990 or 990-EZ.

When do nonprofits not need to file Form 1023?

Gross Receipts Test. Your nonprofit does not need to file Form 1023 with the IRS if its annual gross receipts are normally less than $5,000. “Gross receipts” means the total amount of income your nonprofit receives from all sources during its annual accounting period, without subtracting any costs or expenses.

Why are nonprofit organizations required to file Form 990?

All nonprofit organizations are required to file IRS Form 990. Filing the Nonprofit Form 990 ensures that charitable organizations are accountable to funding sources. Since the 990 is available to the public, it is an easy way for donors and other funding sources to evaluate…

Can a non profit organization qualify for tax exempt status?

If your nonprofit organization makes less than $5,000 per year, you may be able to obtain tax-exempt status from the IRS without filing a Form 1023 application. A few types of nonprofits are in the unique (and enviable) position of being able to qualify as tax-exempt Section 501(c)(3) charitable organizations without applying to the IRS.