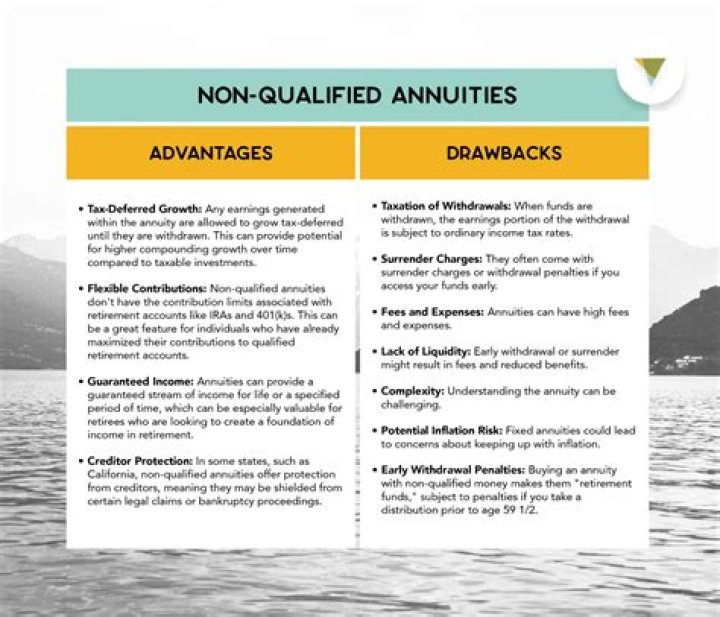

Do non-qualified annuities have RMD?

There are no required minimum distributions for non-qualified annuities. In both those respects, it’s similar to a Roth individual retirement account. Unlike a Roth IRA, however, any earnings withdrawn from non-qualified annuities are taxable at your regular tax rate.

Can you transfer a non-qualified annuity to an IRA?

Non-qualified variable annuities, meaning products set up with after-tax dollars, can’t be rolled over into a traditional IRA. However, non-qualified variable annuities can be rolled over into other non-qualified accounts.

Do I have to take an RMD from my annuity?

Qualified variable annuities held in IRAs are subject to the IRS required minimum distribution (RMD) requirement. At age 72, qualified account owners are required to begin taking RMDs from their IRAs. A 50% penalty on the RMD amount may be assessed if not taken as required.

Can a QLAC withdrawal benefit apply to a commutation withdrawal?

However, a commutation withdrawal benefit offers annuitized income annuities such as an immediate annuity or deferred income annuity, a one-time emergency withdrawal. Commutation Withdrawal Benefits do not apply to a QLAC nor Medicaid annuities.

When does a nonqualified variable annuity become taxable?

When an investor initiates a full surrender of a non-qualified variable annuity (whether receiving annuity payments or taking withdrawals before the annuity starting date), the net gain made over the life of the investment become taxable.

How does a systematic withdrawal work in an annuity?

Systematic withdrawals from an annuity are the automated withdrawal of periodic income payments (via penalty-free withdrawals) throughout the year instead of pocketing the maximum dollar amount once a year. A contract owner can systematically withdrawal annuity income payments via monthly payments, a quarterly payout, or a semi-annual payout.

Are there penalties for withdrawing money from an annuity?

Key Takeaways 1 Withdrawals from annuities can trigger one of two types of penalties. 2 The insurer issuing the annuity charges surrenders fees if funds are withdrawn during the annuity’s accumulation phase. 3 The IRS charges a 10% early withdrawal penalty if the annuity-holder is under the age of 59½.