Does the accumulated earnings tax apply to S corporations?

S corporations don’t have a problem with accumulated earnings because earnings are taxed to S corporation shareholders even if they’re not distributed to them.

Is a distribution from OAA taxable?

Tax Exempt Income in the Other Adjustments Account (OAA), 5. Non-taxable up to the shareholder’s stock basis (i.e. a return of capital), 6. Any distributions in excess of the shareholder’s stock basis will be taxed as a capital gain (i.e. a deemed sale of stock with no basis).

Are corporate retained earnings taxable?

Retained earnings can be kept in a separate account and are tax-exempt until they are distributed as salary, dividends, or bonuses. Salary and bonuses can be deducted from corporate income tax, but are taxed at the individual level.

Do corporations pay taxes on retained earnings?

Retained earnings can be kept in a separate account and are tax-exempt until they are distributed as salary, dividends, or bonuses. Salary and bonuses can be deducted from corporate income tax, but are taxed at the individual level. Dividends are not tax-deductible.

Who is subject to the accumulated earnings tax?

The accumulated earnings tax imposed by section 531 shall apply to every corporation (other than those described in subsection (b)) formed or availed of for the purpose of avoiding the income tax with respect to its shareholders or the shareholders of any other corporation, by permitting earnings and profits to …

What is the maximum amount of accumulated earnings that a corporation is allowed to accumulate without regard to business needs before the accumulated earnings tax is imposed?

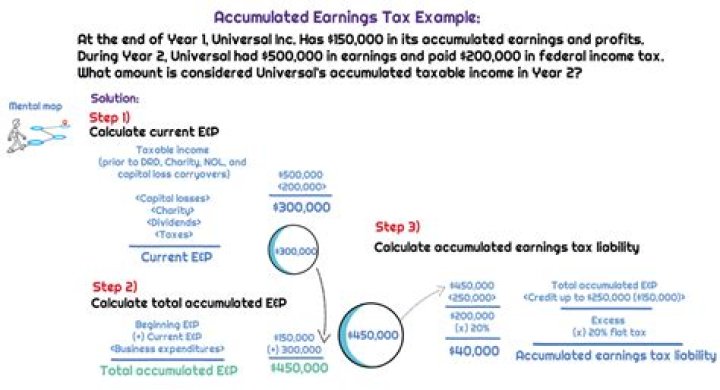

Virtually any corporation can accumulate up to $250,000 in retained earnings without becoming subject to tax on the accumulated funds. In addition, as long as the accumulation is related to a reasonable business need, then it will not be subject to tax.

How can a corporation avoid paying accumulated earnings tax?

If a company does not distribute any dividends by keeping a portion of retained earnings as accumulated earnings, shareholders are able to avoid this tax. Companies that retain earnings typically experience higher stock price appreciation.

How is accumulated earnings calculated?

Accumulated earnings and profits (E&P) are net profits a company has available after paying dividends. This figure is calculated as E&P at the beginning of the year plus current E&P minus distributions to shareholders during the current period.

How is accumulated taxable income calculated for a corporation?

Generally, a corporation’s “accumulated taxable income” is calculated as follows: What is “Accumulated Earnings Credit”? Accumulated earnings credit is the greater of the following two amounts: $250,000 (or $150,000 for personal service corporations) less the amount of accumulated earnings and profits at the end of last tax year; or

How are accumulated earnings taxed in the US?

S corporations are not liable for the accumulated earnings tax since earnings in these firms are taxed to investors and shareholders whether the company makes distributions to them or not. The offers that appear in this table are from partnerships from which Investopedia receives compensation.

Who is liable for the accumulated earnings tax?

S corporations are not liable for the accumulated earnings tax since earnings in these firms are taxed to investors and shareholders whether the company makes distributions to them or not.

How is income taxed in a C corporation?

Although the new 21% rate is tempting, C corporations are subject to double taxation. Corporate income is taxed once at the entity level and again when it is distributed to shareholders as dividends.