How are gambling winnings tracked?

You Have to Report All Your Winnings Whether it’s $5 or $5,000, from the track or from a gambling website, all gambling winnings must be reported on your tax return as “other income” on Schedule 1 (Form 1040). If you win a non-cash prize, such as a car or a trip, report its fair market value as income.

How do you keep track of gambling winnings and losses?

Recordkeeping. To deduct your losses, you must keep an accurate diary or similar record of your gambling winnings and losses and be able to provide receipts, tickets, statements, or other records that show the amount of both your winnings and losses.

What do you need to know about gambling winnings?

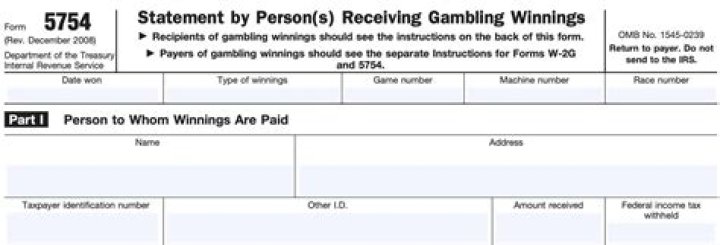

Gambling Winnings. A payer is required to issue you a Form W-2G.pdf, Certain Gambling Winnings, if you receive certain gambling winnings or have any gambling winnings subject to federal income tax withholding. You must report all gambling winnings on your Form 1040.pdf as “Other Income” (line 21), including winnings that aren’t reported on…

Where can I find 419 gambling income and losses?

419 Gambling Income and Losses 1 Gambling Winnings. A payer is required to issue you a Form W-2G, Certain Gambling Winnings if you receive certain gambling winnings or have any gambling winnings subject to federal income 2 Gambling Losses. 3 Nonresident Aliens. 4 Recordkeeping. 5 Additional Information. …

Do you have to report gambling winnings on Form 1040?

You must report all gambling winnings as “Other Income” on Form 1040 or Form 1040-SR (use Schedule 1 (Form 1040) PDF), including winnings that aren’t reported on a Form W-2G PDF. When you have gambling winnings, you may be required to pay an estimated tax on that additional income.

Do you have to pay taxes on winnings from gambling?

Gambling might be an enjoyable pastime for some and it might provide a nice adrenaline rush when you win, but your winnings are subject to federal income tax, and possibly to state taxes as well. The IRS requires that you report the money as income, although it does allow you to claim a deduction for at least some of your losses.