How are shareholder distributions taxed in a S corporation?

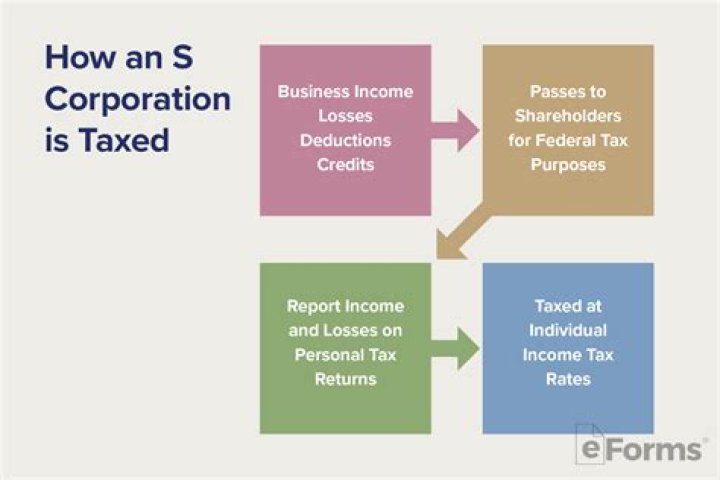

S corp shareholder distributions are the earnings by S corporations that are paid out or “passed through” as dividends to shareholders and only taxed at the shareholder level. Unlike a partnership, an S corporation is not subject to personal holding company tax or accumulated earnings tax.

How does the IRS look at shareholder distributions?

The IRS will look at the number of hours you work, and your duties, responsibilities, education and training to confirm that your salary reflects your job performance. If you receive overly high distributions, especially if your paycheck is unusually low, the IRS will reclassify the excess distribution as payroll.

What’s the difference between a shareholder and a stakeholders?

When it comes to investing in a corporation, there are shareholders and stakeholders. While they have similar sounding names, their investment in a company is quite different. Shareholders are always stakeholders in a corporation, but stakeholders are not always shareholders.

Why do shareholders decrease their stock basis for distributions?

Shareholders decrease their stock basis for distributions, items of loss and deductions, nondeductible expenses and certain non-excess depletion deductions. The income tax regulations provide a specific order in which these items are applied to adjust stock basis.

Do you have to distribute profits to shareholders?

An S corporation’s unique tax status dictates that it must allocate the profits to the shareholders each year, but there is no requirement for the company to distribute them. State law can determine whether the corporation holds on to the money as working capital or distributes the profits. S corporations begin as traditional C corporations.

When does a corporation pay a shareholder a dividend?

When a corporation pays a shareholder a dividend or distribution, the payment needs to be categorized not as an expense or a tax deduction but a draw, or reduction, in retained earnings.

When do shareholders have to take equal distributions?

The answer depends on what is meant by unequal distributions. If unequal means not equal to each other shareholders, that may be acceptable if there are more than two shareholders with varying percentages of the corporation as stock.

What happens if a shareholder contributes$ 100, 000 to a s-Corp?

If a shareholder contributes $100,000 to their S-Corp and later distributes $50,000 to help pay their personal bills they run into a serious tax problem. The $50,000 is likely subject to the reasonable compensation rules stated above.

Can a corporation distribute property to a shareholder?

As a general rule, however, assets that have basis in excess of FMV should not be distributed to a shareholder because the potential loss cannot be used by either the corporation or the distributee shareholder. To summarize, distribution of the equipment to B would cause A&B to recognize ordinary income of $20,000.

Can a trust be a shareholder of a S corporation?

S corporations are subject to special limitations on the number and type of shareholders. For example, a corporation or institutional investor may not be a shareholder in an S corporation because Subchapter S of the Code only permits individuals and certain trusts to be S corporation shareholders.

Is the C corporation income taxed at the corporate level?

C Corporation income is first taxed at the corporate level and then, when distributed to the shareholders, taxed again as a dividend. When an S Corporation distributes its income to the shareholders, the distributions are tax-free. Or are they? As one of my partners often reminds me, the answer to every tax questions is “It depends.”

How are distributions determined if S corporation does not have ae & P?

If an S Corporation does not have AE&P, the taxability of distributions is determined solely by reference to the shareholder’s stock basis. Any distributions will be a tax-free reduction of the shareholder’s basis. Any distribution in excess of the shareholder’s stock basis is treated as capital gain from the deemed disposition of stock.

How is a C Corp dividend reported to shareholders?

A regular C corporation distributing its earnings out of retained earnings is considered a dividend. C corp shareholders receive Form 1099-DIV and they will, in turn, report the dividend on their individual federal tax return. S corporations, in general, do not make dividend distributions.

Can a corporation claim a loss on a property distribution?

If the FMV of the distribution is less than the corporation’s tax basis, it cannot claim a loss because of the property distribution. Instead it must decrease current E&P by the adjusted basis of the property. When the shareholder receives the property, then the adjusted basis in the property is the property’s FMV, not the corporation’s basis.

How often do companies pay distributions to shareholders?

Distributions are allocations of capital and income throughout the calendar year. When a corporation earns profits, it can choose to reinvest funds in the business and pay portions of profits to its shareholders. Shareholders can receive distributions on a regular basis, such as monthly, quarterly, or annually.

What’s the rule for disproportionate distribution in S-corporations?

S-Corporations with Disproportionate Distribution The general rule is that distributions from S-Corporations to shareholders should be proportional to each shareholder’s ownership interest. By Eric Gros-Dubois Jan

Where does S corporation keep its undistributed earnings?

An S corporation keeps its undistributed earnings in the accumulated adjustments account (AAA). When it distributes from this account at a later date, the distributions are tax-free for the shareholders because they have already paid the taxes at the time of income accrual.

Can a majority shareholder refuse to declare a dividend?

But since there is no duty to either sell the company or declare a dividend on the part of the majority Shareholder, it is typical in such situations for the minority Shareholder to own essentially worthless stock for years, watching salary and bonuses be paid, while the majority Shareholder refuses to declare dividends, or sell the company.

What happens to minority shareholders when a company is sold?

If the company is sold, the minority shareholder must receive the same price per share as the majority shareholder. Secondly, if a dividend is declared, the minority shareholder must receive the same dividend per share as the majority shareholder.

Can A S-corporation have two equal shareholders?

However, there is an exception known as the “timing difference.” This exception, however, will only apply to instances in the following examples: (1) A S-Corporation has two equal shareholders, X and Y, and are each entitled to equal distributions.

Can A S corporation be classified as salary?

The IRS offers no hard-and-fast rules for estimating reasonable compensation, and thorough documentation to support the S corporation’s classification is key. The IRS is cracking down on S corporations that misclassify payments to shareholder-employees as distributions — rather than salary expense.

Why do S corporations classify payments as distributions instead of salary?

The IRS is cracking down on S corporations that misclassify payments to shareholder-employees as distributions — rather than salary expense. Some S corporations do this in an effort to minimize payroll taxes, which in many cases will now be more significant because of the additional 0.9 percent Medicare tax.

What was the profit of the S Corp?

The total profit of the S Corp before any owner wages was $220,000. The owner, Tony Stark, paid himself a reasonable compensation of $120,000. This brought business income down to $100,000. If Mr. Stark gives himself a $10,000 S Corp bonus, his wages go up to $130,000, and business income goes down to $90,000.