How is a draw from an S Corp taxed?

Owner’s draw in an S corp Since an S corp is structured as a corporation, there is no owner’s draw, only shareholder distributions. A shareholder distribution is a non-taxable event, and if you try to replace your regular, taxed, W-2 income with non-taxable distributions, the IRS will catch you.

How do you pay yourself from S Corp?

Here’s a simple strategy that you can try, and it’s called the 60/40 rule:

- Pay 60% of your business income to yourself in the form of employee salary.

- Pay yourself 40% of your business income in the form of distributions.

How does a s Corp pay income taxes?

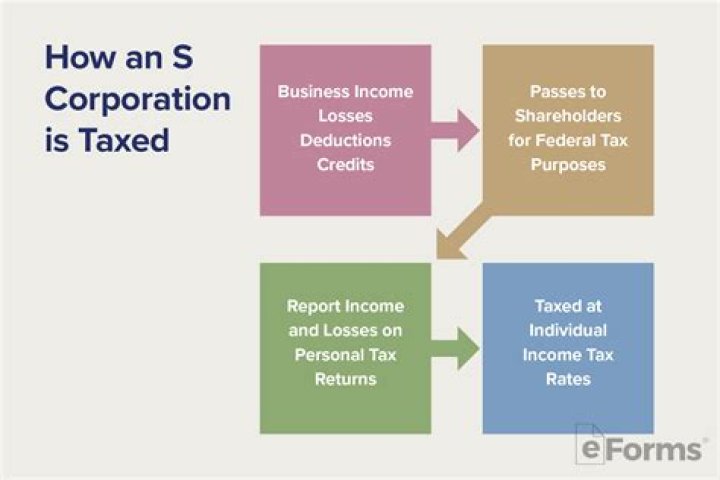

An S-Corp does not pay income taxes on its own because the S-Corp, for income tax purposes, has no income. It’s all been distributed to shareholders via Schedule K-1. The shareholders then enter the information off their Schedule K-1’s in their own income tax returns.

Do you have to pay taxes on a C Corp draw?

Owners can deduct their salaries as a business expense. This approach is especially useful in a C corp because a draw or distribution would come as a dividend, which is subject to double taxation. The first tax hit comes when the profits are taxed. The second is when your dividend gets reported as income. Double trouble? No thanks!

How are shareholder distributions taxed in a S corporation?

S corp shareholder distributions are the earnings by S corporations that are paid out or “passed through” as dividends to shareholders and only taxed at the shareholder level. Unlike a partnership, an S corporation is not subject to personal holding company tax or accumulated earnings tax.

Why are owner’s draws good for S Corp?

Owner’s draws can give S corps and C corps extra tax savings The IRS tax implications are huge if you’re an S corp or a C corp. The biggest reason is that draws, dividends, and distributions are typically not subject to payroll taxes. For an S corp, only your wages are subject to IRS payroll taxes — assuming you’re also an employee.