How much capital gain can I exclude from my tax return?

If you have a capital gain from the sale of your main home, you may qualify to exclude up to $250,000 of that gain from your income, or up to $500,000 of that gain if you file a joint return with your spouse.

What’s the maximum exclusion for capital gains on a home sale?

The result is the amount of the gain you can exclude from your taxable income. For example, you might have lived in your home for 12 months, then you had to sell it for a qualifying reason. You’re not married. Twelve months divided by 24 months comes out to .50. Multiply this by your maximum exclusion of $250,000.

When do you get the 250k / 500K exclusion?

The IRS chomps away at the $250k/$500k exclusion amount based on a proration of the amount of time that you’ve held the property as a rental since January 1, 2009 (note that it goes back more than 5 years now to look at the use period).

How to qualify for the 250, 000 home sale exclusion?

1 The Two Year Ownership and Use Rule. Here’s the most important thing you need to know: To qualify for the $250,000/$500,000 home sale exclusion, you must own and occupy the 2 If You are Not Living in the Home. 3 The Home Must Be Your Principal Residence. 4 $500,000 Exclusion for Married Couples. …

Do you qualify for the$ 250, 000 home sale exclusion?

For married homeowners filing jointly, up to $500,000 of gain is excluded from income. To qualify for the exclusion, the home must have been used as a main home for two years out of the prior five years before the sale. For details, see The $250,000/$500,000 Home Sale Exclusion. At the time you inherit a home, you won’t qualify for this exclusion.

When do you qualify for the 500, 000 tax exclusion?

If your spouse dies and you subsequently sell your home, you qualify for the $500,000 exclusion if the sale occurs within two years after the date of death and the other requirements discussed above were met immediately before the date of death. Talk to a Tax Attorney.

If your gain is more than $125,000, you would include only the amount over $125,000 as taxable income on your tax return. If you realize a $150,000 gain, you would report and pay taxes on $25,000. If your gain is equal to or less than $125,000, you can exclude the entire amount from your taxable income.

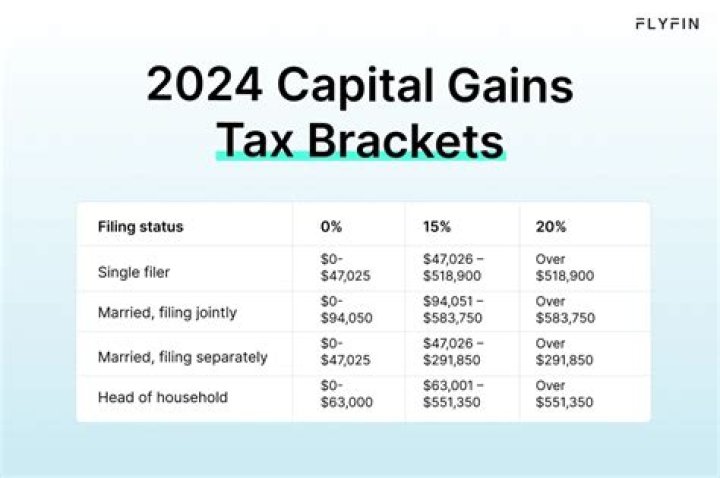

What are the tax rates for capital gains?

Capital gains tax rates on most assets held for less than a year correspond to ordinary income tax brackets (10%, 12%, 22%, 24%, 32%, 35% or 37%). What is short-term capital gains tax? Short-term capital gains tax is a tax on profits from the sale of an asset held for one year or less.

What does it mean when you have a capital gain?

A capital gain happens when you sell or exchange a capital asset for a higher price than its basis. The “basis” is what you paid for the asset, plus commissions and the cost of improvements, minus depreciation.

How do you calculate capital gain on sale of stock?

The difference between the buying price and the selling price is your capital gain or loss. The formula is Sale Price – Cost Basis = Capital Gain. For example, suppose you purchased 100 shares of stock for $1 each for a total value of $100. After three months, the stock price rises to $5 per share, making your investment worth $500.

What is capital gains tax and when are you exempt?

The capital gains tax is what you owe for the money you’ve made selling certain assets. Here’s what you need to know about the current rate and what can be exempt. Author: Steve Fiorillo. Updated: Feb 20, 2020 2:38 PM EST. Original:

Is there a capital gains tax exemption in Israel?

Capital Gains tax in Israel: The capital gains exemption which allowed an Israeli tax payer to sell a residential property once every four years with a full tax relief was canceled on January 1, 2014. The only tax exemption that remains in force is in a case of an Israeli individual who owns a single home which is his only property in Israel.

How much can you sell your home without paying capital gains tax?

When you sell your primary residence, $250,000 of capital gains (or $500,000 for a couple) are exempted from capital gains taxation. This is generally true only if you have owned and used your home as your main residence for at least two out of the five years prior to the sale.

Can a spouse exclude capital gains in a divorce?

Situation 2: One spouse is buying out the other and staying in the home. “Sometimes in the divorce, one spouse will buy the other spouse’s half of the house,” Katt said. When the time comes for the ex-spouse who took full ownership to sell the house, they’ll only be able to exclude $250,000 of capital gains.

How are capital gains taxed for married couple?

Now, to qualify for the $500,000 exemption, a married couple must meet the following conditions: If even after all of the generous tax breaks, your gain exceeds your exemption threshold of either $250,000 or $500,000, the remainder of your gain will be taxable at a rate of 0%, 15%, or 20% dependent on your tax bracket.

Can you exclude gain on sale of home on tax return?

Alternatively, a taxpayer can elect to include the gain from a sale by reporting it on his or her tax return. For example, someone who realizes gains on the sale of two principal residences within two years can exclude the gain on only one.

How much money did the IRS fail to audit?

According to a recent report by the Treasury Inspector General for Tax Administration (TIGTA), due to a lack of resources, the IRS failed to audit more than 897,000 wealthy individuals who skipped out on filing tax returns over a three‑year period – and these individuals owed nearly $46 billion in taxes.

Do you have to pay taxes on ill gotten gains?

Here’s one upshot to declaring ill-gotten gains: If taxes are paid on it initially, and restitution is part of any settlement or judgment, that restitution is then tax-deductible, says Moskowitz. If you decide to disclose your illegal loot, make sure to do it with the assistance of a tax attorney, not any old accountant.

Why does the IRS say I owe more taxes?

You paid your taxes—but now the IRS says that you owe more. Each year, the IRS sends out millions of notices requesting additional payments from taxpayers who made math errors on their returns…neglected to report certain income…claimed tax credits or deductions that they were not entitled to…or made other mistakes.

Do you have to pay tax on capital gains on sale of primary residence?

Due to the exclusion and due to the home being their primary residence, they didn’t have to pay any tax on this gain. Even a single taxpayer selling their primary residence for such a profit wouldn’t have to pay any capital gains tax because they would still fall under the lower exclusion limit.

When do capital gains get excluded from IRC 1400z-2?

Effective December 22, 2017, IRC 1400Z-2 provides a temporary deferral of inclusion in gross income for capital gains invested in Qualified Opportunity Funds, and permanent exclusion of capital gains from the sale or exchange of an investment in the Qualified Opportunity Fund if the investment is held for at least 10 years.