Is cash-out of a mortgage refinance taxable?

The IRS doesn’t view the money you take from a cash-out refinance as income – instead, it’s considered an additional loan. You don’t need to include the cash from your refinance as income when you file your taxes.

How do you report interest paid on a mortgage?

Use Form 1098, Mortgage Interest Statement, to report mortgage interest (including points, defined later) of $600 or more you received during the year in the course of your trade or business from an individual, including a sole proprietor. Report only interest on a mortgage, defined later.

How much can you deduct on a cash out mortgage?

With a cash-out refinance, you cannot deduct the total amount of money you paid on points during the year you did the refinance, but you can take smaller deductions throughout the life of the loan. So if you purchase $2,000 worth of mortgage points on a 15-year refinance, you can deduct about $133.33 per year for the duration of the loan.

What’s the interest rate on a cash out mortgage refinance?

Using a cash-out refinance to pay off credit card debt may be the better move if you’re burdened by high-interest debt. “The average credit card rate is around 16 percent and mortgage rates are sitting at around 3 or 4 percent,” explains DiBugnara. It’s also important to note that there are other limits to mortgage interest deductions.

Are there any tax implications for a cash out refinance?

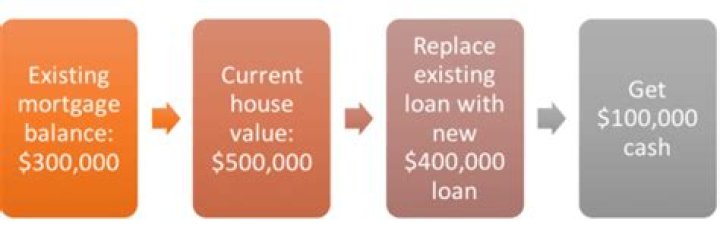

However, this isn’t “free money,” and there are tax implications. A cash-out refinance replaces your current mortgage with a larger one. The larger, new one includes the balance of the current mortgage, the cash (equity) you received and any closing costs rolled into the new mortgage.

Can a cash out mortgage be used to pay off credit card debt?

If you use it to pay off your credit card debt, you can deduct the interest you paid on only your original balance, or $60,000. Using a cash-out refinance to pay off credit card debt may be the better move if you’re burdened by high-interest debt.