Is land depreciated over its useful life?

Land is not depreciated because land is assumed to have an unlimited useful life. Other long-lived assets such as land improvements, buildings, furnishings, equipment, etc. have limited useful lives. Therefore, the costs of those assets must be allocated to those limited accounting periods.

How is landscaping depreciated?

The general IRS rules says to depreciate over 15 years items that are “inextricably associated with the land” and increase the value of the land. Landscaping is said not to have a useful life of its own, so it’s not depreciated as a land improvement.

How long do you depreciate land for?

27.5 years

The Internal Revenue Service (IRS) allows building owners the opportunity under the Modified Accelerated Cost Recovery System (MACRS) to depreciate certain land improvements and personal property over a shorter period than 39 or 27.5 years.

Can land ever be depreciated?

Land can never be depreciated. Since land cannot be depreciated, you need to allocate the original purchase price between land and building. You can use the property tax assessor’s values to compute a ratio of the value of the land to the building.

Is landscaping a fixed asset?

A special item is the ongoing cost of landscaping. This is a period cost, not a fixed asset, and so should be charged to expense as incurred.

Can we charge depreciation on land?

Depreciation means decrease in value of property through wear, deterioration or obsolescence. (Webster’s New Word Dictionary). In that sense, land cannot depreciate. Depreciation is allowable only on the value of superstructure on the land and not on the value of land.”

Does land have depreciation?

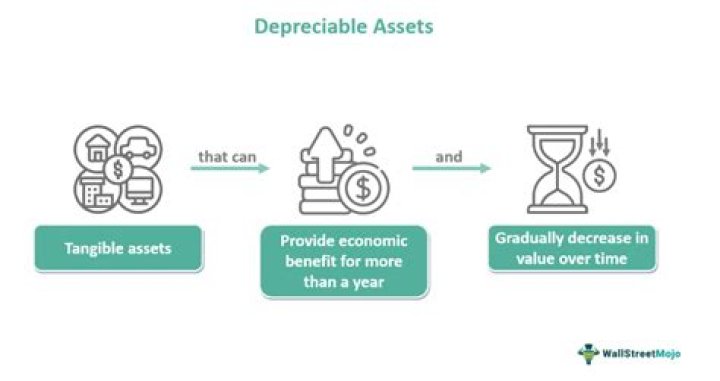

Land, although a tangible fixed asset, does not depreciate. Land cannot get deteriorated in its physical condition; hence we cannot determine its useful life. It is almost impossible to calculate land depreciation.