Is manufacturing included in COGS?

Cost of goods sold (COGS) is the cost of acquiring or manufacturing the products that a company sells during a period, so the only costs included in the measure are those that are directly tied to the production of the products, including the cost of labor, materials, and manufacturing overhead.

Are manufacturing costs the same as COGS?

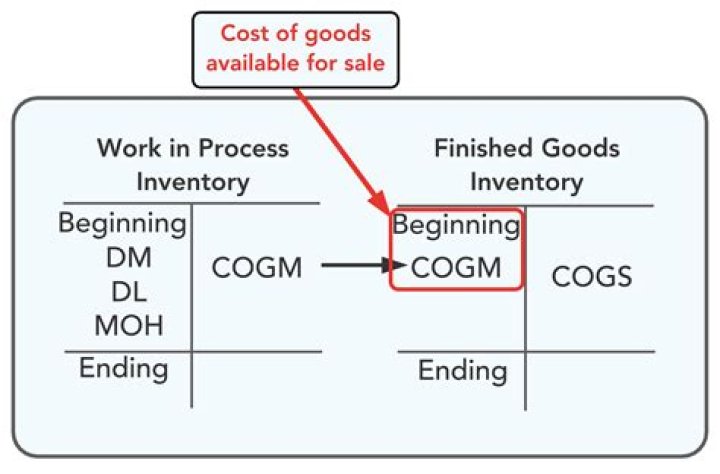

The cost of goods manufactured is not the same as the cost of goods sold. Goods manufactured may remain in stock for many months, especially if a company experiences seasonal sales. Conversely, goods sold are those sold to third parties during the accounting period.

How do you add cost of goods manufactured?

What Does Cost of Goods Manufactured Mean? The cost of goods manufactured equation is calculated by adding the total manufacturing costs; including all direct materials, direct labor, and factory overhead; to the beginning work in process inventory and subtracting the ending goods in process inventory.

Is Labor an expense or COGS?

Direct labor costs are part of cost of goods sold or cost of services as long as the labor is directly tied to production. As a result, direct costs are factored into gross profit through COGS or COS. However, not all labor costs are included in COGS.

What’s the difference between COGM and cogs?

Cost of goods manufactured are the production costs incurred on finished goods produced in a specific accounting period. Cost of goods sold are the production costs incurred on goods actually sold in a specific accounting period.

How is the cost of goods manufactured budget related to the cost of goods sold budget?

It is prepared to calculate the manufacturing costs that are expected to be incurred on budgeted finished goods. The cost of goods manufactured budget is based on direct material purchases budget, direct labor cost budget and factory overhead budget.

How do you calculate manufacturing cost of goods sold?

The calculation of the cost of goods sold for a manufacturing company is:

- Beginning Inventory of Finished Goods.

- Add: Cost of Goods Manufactured.

- Equals: Finished Goods Available for Sale.

- Subtract: Ending Inventory of Finished Goods.

- Equals: Cost of Goods Sold.

What is the formula to calculate COGS for a manufacturing company?

The calculation of the cost of goods sold for a manufacturing company is: Beginning Inventory of Finished Goods. Add: Cost of Goods Manufactured. Equals: Finished Goods Available for Sale.

When to add cost of goods sold to cogs?

Keep a running log of the cost of goods made for everything you have for sale. When it sells, take that cost out of your inventory bucket, and add it into your COGS total for the year. Easy peasy. You should still verify this COGS total with a physical count before you do your tax return!

What kind of expenses should be included in a cog?

Separate your expenses because COGS should only include certain outgoings. The sale income from manufactured goods; and The sale income from any resold goods. Income from any other services that do not include selling goods. Direct labor costs. SG&A (Sales, General, and Admin costs), including rent, utilities, and e-commerce fees; and

Why is the value of cogs important in manufacturing?

The value of COGS is important for several reasons: Helps to Set Profitable Pricing – In complex manufacturing systems, costing each step of production is a challenge. As a result, a wrong calculation, or series of calculations, can reduce the gap between COGS per unit and unit price.

How are cogs calculated on a business tax form?

FIFO (“First-In, First-Out”) assumes that the first goods bought are the first goods sold. S LIFO (“Last-In, First-Out”) assumes that the first goods bought are the first goods sold. COGS calculation is included in the business tax form for every business type that sells products.