Is selling a gift taxable?

The Internal Revenue Service (IRS) doesn’t consider gifts to be income, even if the gift is cash. You would only owe this tax if you decided to give the gift away, or if you sold it for significantly less than its fair market value.

How is gifted Stock taxed when sold?

When gifting stock to a relative, there is no tax impact for the donor or the relative receiving the shares. If the gift exceeds that amount, they would have to file an estate and gift tax return, but again, there would be no tax implications unless the gift exceeded their lifetime gift and estate tax exemption.

How are gifts and related party transactions taxed?

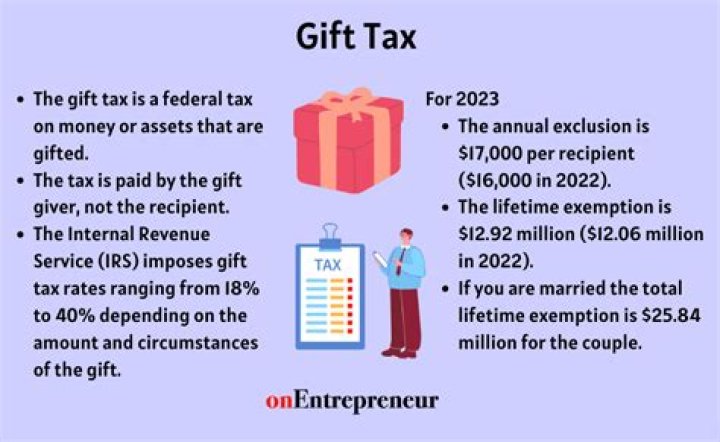

Tax Rules for Gifts and Related Party Transactions. According to federal taxation rules, the gift giver is taxed and the recipient is not taxed. Gift taxes are filed under form 706. The donor may exclude the first initial $14,000* (2013) under the single/head of household/married filing jointly status.

What are tax considerations when you sell gift property?

The IRS considers that you would have given a gift worth $500,000 to the buyer if you sold your grandmother’s artwork valued at $1 million for just $500,000. That’s $485,000 more than your annual $15,000 exclusion, so you’d either have to pay the gift tax on that balance or subtract the $485,000 from your $11.58 million lifetime exemption.

What are the tax consequences of related party sales?

Related party sales generally create negative tax consequences for sellers including recharacterizing capital gains as ordinary income, denying installment sales reporting, disallowing realized losses and restricting the use of like-kind exchanges.

How are gifts received exempt from income tax?

According to income tax laws, the value of all the gifts received by a person during a year is fully exempt, as long as the total of such gifts does not exceed Rs 50,000 in a year. If the value of all the gifts taken together exceeds Rs 50,000, then, the aggregate of the gifts received become taxable without any threshold exemption.