Is there a difference between 1099 and 1099-Misc?

The 1099-R refers to retirement income, while the 1099-MISC is for independent contractors and freelancers who perform a service for someone during the tax year. These are only two of the many varieties of the form that exist, each to report a specific type of income.

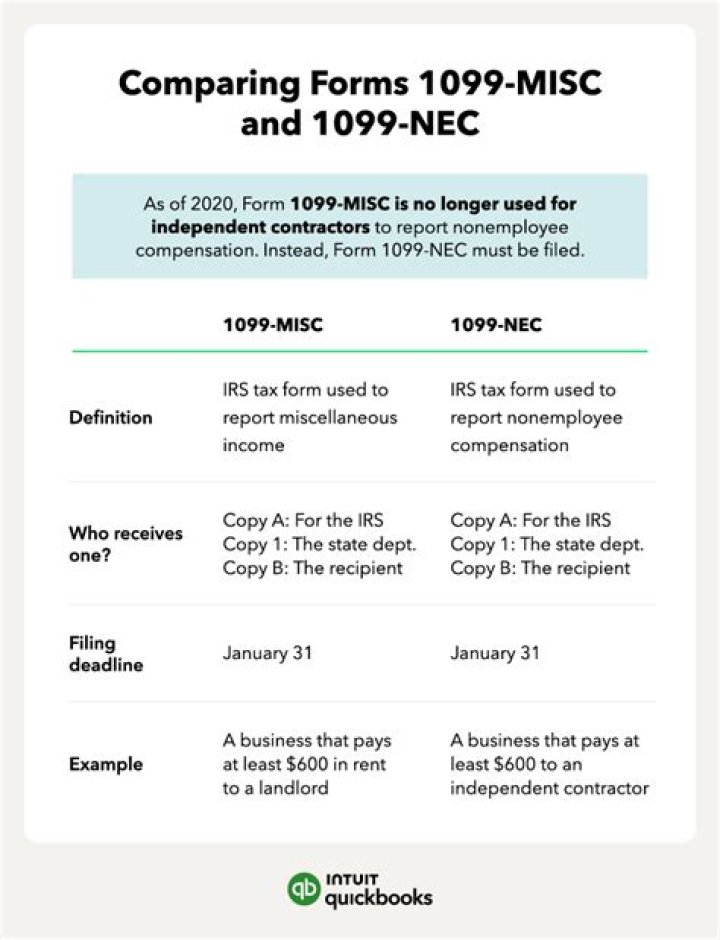

Who gets a 1099-MISC VS 1099-NEC?

Form 1099-MISC differs from Form 1099-NEC in one distinct way. A business will only use a Form 1099-NEC if it is reporting nonemployee compensation. If a business needs to report other income, such as rents, royalties, prizes, or awards paid to third parties, it will use Form 1099-MISC.

What is the difference between NEC and misc 1099?

The 1099-NEC will be the exclusive form business taxpayers will use to report payments to independent contractors starting from the tax year 2020. This means that Form 1099-NEC will replace box 7 on Form 1099-MISC, which is where clients used to report non-employee compensation.

What do you need to know about Form 1099 MISC?

A Form 1099-MISC will have your Social Security number or taxpayer identification number on it, which means the IRS will know you’ve received interest — and it will know if you don’t report that income on your tax return. Do you pay taxes on a 1099-MISC?

How to report payments to an attorney on 1099-MISC?

To report payments to an attorney on Form 1099-MISC, you must obtain the attorney’s TIN. You may use Form W-9, Request for Taxpayer Identification Number and Certification, to obtain the attorney’s TIN.

Do you have to report scholarships on Form 1099-MISC?

Scholarships. Do not use Form 1099-MISC to report scholarship or fellowship grants. Scholarship or fellowship grants that are taxable to the recipient because they are paid for teaching, research, or other services as a condition for receiving the grant are considered wages and must be reported on Form W-2.

Do you have to file Form 1099 Misc for nonqualified deferred compensation?

Nonqualified deferred compensation (box 14). You must also file Form 1099-MISC for each person from whom you have withheld any federal income tax (report in box 4) under the backup withholding rules regardless of the amount of the payment.