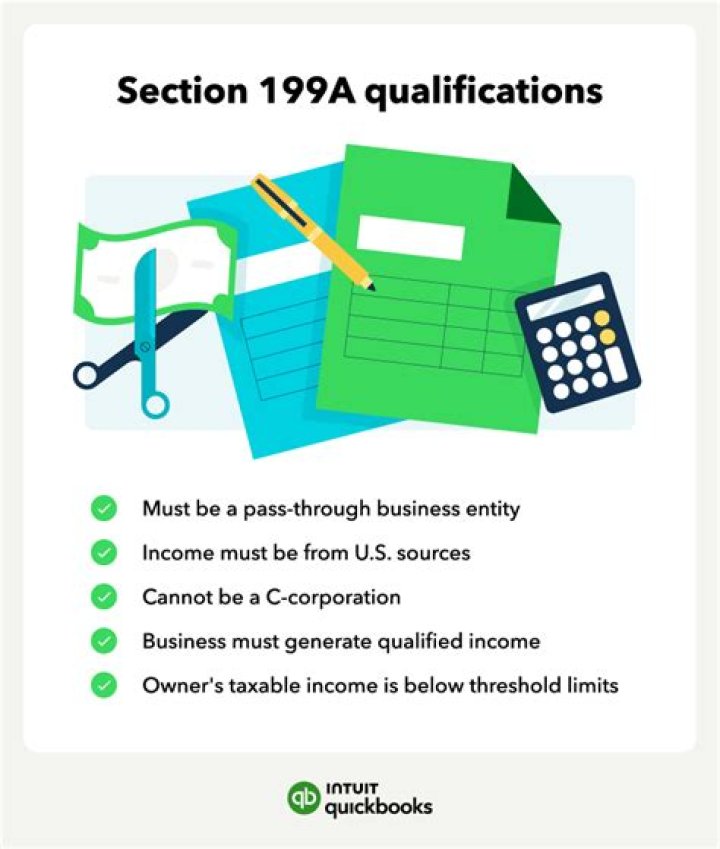

What activities qualify for 199A?

Section 199A of the Internal Revenue Code provides many owners of sole proprietorships, partnerships, S corporations and some trusts and estates, a deduction of income from a qualified trade or business.

Do musicians qualify for 199A?

Musicians and other performing artists with taxable income below $157,500 for single filers or $315,000 married filing jointly are eligible for the full 20% deduction. The QBI deduction will then phase out for income above these levels over the next $50,000 (single) or $100,000 (married) of household income.

Do musicians qualify for the QBI deduction?

While most musicians who file schedule C will be eligible for this deduction, high earners – those making over $157,500 single or $315,000 married – will see this deduction phased out to zero, because they are considered a Specified Service Trade or Business (SSTB).

How much can you deduct on section 199A?

Mary’s Section 199A deduction is the lesser of 20% of her taxable income less net capital gain ($100,000 of Schedule C income plus $1,000 QDI less $12,000 standard deduction less $1,000 “net capital gain” – in this case, her QDI – equals $88,000. $88,000 X 20% = $17,600) or 20% of her QBI ($100,000 X 20% = $20,000).

Is the section 199A deduction a compliance challenge?

But those who have started to address what’s required to qualify for the deduction may be realizing that 199A is both a tax benefit and a compliance challenge. Unlike a simple reduction in a tax rate, which is clean and relatively easy to calculate, this deduction is complex.

When did the final regulations come out for section 199A?

The government issued final regulations for this deduction in February 2019. But those who have started to address what’s required to qualify for the deduction may be realizing that 199A is both a tax benefit and a compliance challenge.

What is the domestic production activities deduction under section 199A?

Section 199A(g) provides a deduction for Specified Cooperatives and their patrons similar to the deduction under former section 199, which was known as the domestic production activities deduction. Section 199A(g) allows a deduction for income attributable to domestic production activities of Specified Cooperatives.