What happens to old mortgage when refinance?

When you refinance, you replace one mortgage with another. Funds from the new mortgage will be used to repay the old loan. Refinancing also means that loan servicing may be transferred from one servicer to another. This is the time when you need to work carefully with your new lender and your old lender.

Do both borrowers have to sign the initial closing disclosure?

All parties on the loan (and in some cases even spouses that aren’t on the loan) must e-sign the Initial CD to close on time. Federal law mandates the Initial Closing Disclosure be signed three business days before closing. A delay in signing the Initial CD will result in a delayed closing.

Who signs the closing disclosure on a refinance?

lender

Initial closing disclosure review The initial closing disclosure is a written document from the lender notifying the borrower of loan terms, loan amount, projected payments, fees, and closing conditions. Legally, your lender must provide you this document three days prior to signing your loan documents.

What does signing a loan disclosure mean?

After choosing a lender and running the gantlet of the mortgage underwriting process, you will receive the Closing Disclosure. This means that it contains the locked-in costs of your loan and the specific amount you’ll need to pay at closing. You’ll receive this document three days before your scheduled loan closing.

What happens after signing loan disclosures?

After the lender receives the signed Closing Disclosure from all borrowers, they can begin preparing loan documents. Once the loan documents are prepared, they are delivered to the escrow company. Signing. Signing typically takes place 1-2 days before closing.

Should I pay my old mortgage if refinancing?

When you refinance, you typically don’t make a mortgage payment on the first of the month immediately after closing. Your first payment is due the next month. In a refinance, your original loan is paid off at closing. If you close July 15, you will have already made your July mortgage payment.

Should I refinance after 10 years?

If your mortgage is only a couple of years old, and you can refinance to a significantly lower interest rate, lengthening your mortgage term inflicts only minimal damage. If you are 10 years or more into a 30-year loan, consider refinancing to a shorter-term loan, say, 20, 15 or 10 years.

Do I get my escrow balance back when I refinance?

When you refinance a loan, the original escrow account remains with the old loan. All the property tax and insurance payments you have made to that account, since the last payment was made, will be returned to you, usually within 45 days via wire transfer or check.

How can I skip two payments on a refinance?

In order to skip two mortgage payments, you’d need to close your refinance sometime prior to the 15th of the month, before the payment on the old mortgage is due (using the grace period to delay and avoid payment).

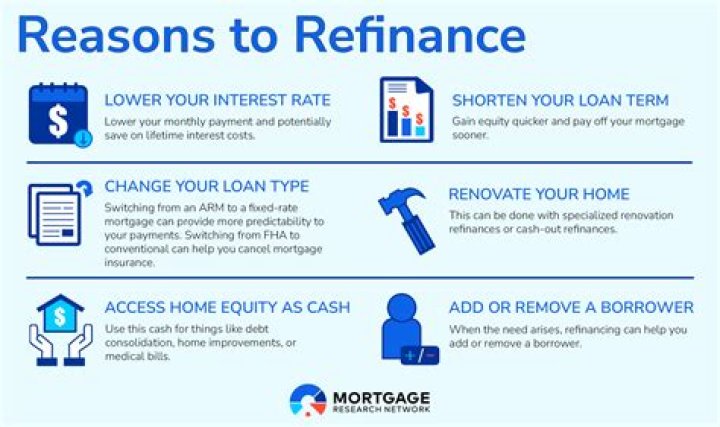

What does it mean when you refinance your mortgage?

A mortgage refinance refers to the process of getting a new loan for your home. When you refinance, the new mortgage loan pays off the old one, so you’re left with just one loan and one monthly payment. There are a few reasons people refinance their homes.

Is it worth it to refinance a 30 year mortgage?

If, for example, you have been making payments for seven years on a 30-year mortgage and refinance into a new 30-year loan, remember you will be making seven extra years of loan payments. The refinance may still be worthwhile, but you should roll those costs into your calculations before making a final decision.

How old do you have to be to refinance your mortgage?

We asked Scott Sheldon, a Credit.com contributor and a senior loan officer at Sonoma County Mortgages, what he thought. He said he can see the reader’s point, but the decision is neither a slam-dunk nor based solely on age. By our calculation, our reader would have been 57 when he got that mortgage and therefore 87 when it is fully paid off.

How long does it take to get mortgage refinance approval?

Obtaining a mortgage refinance approval requires coordination of several different companies, all with the goal of providing you with a new loan for hundreds of thousands of dollars. It’s a process that usually takes at least 7 to 10 business days and can take months depending on how busy the companies are and how complicated the new mortgage is.