What is 965 A income?

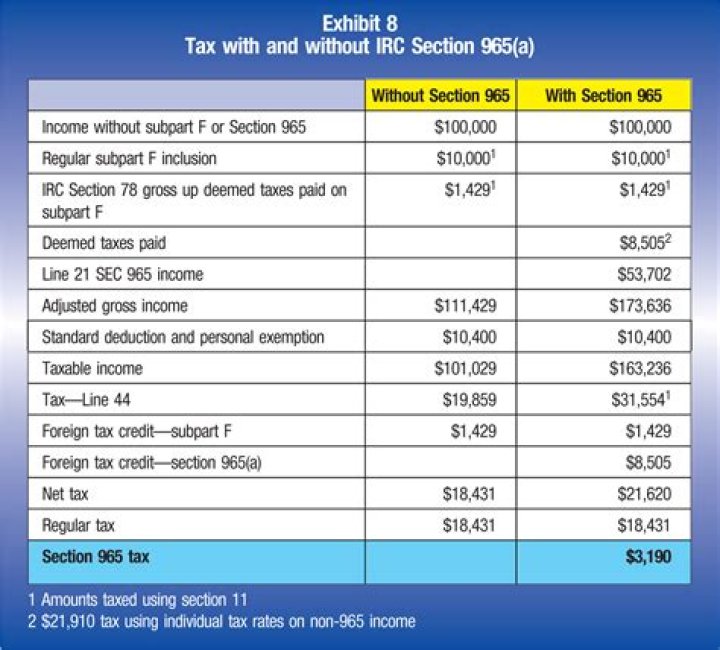

What is section 965? Section 965 requires United States shareholders (as defined under section 951(b)) to pay a transition tax on the untaxed foreign earnings of certain specified foreign corporations as if those earnings had been repatriated to the United States.

Who Must File form 965 A?

Any individual taxpayer (or taxpayer taxed like an individual) who has a net 965 tax liability for any tax year or has any net 965 tax liability remaining unpaid at any time during a tax year must file this form.

What is a Form 965?

More In Forms and Instructions Form 965-A is used by individual taxpayers and entities taxed like individuals to report a taxpayer’s net 965 liability, for each tax year in which a taxpayer must account for section 965 amounts.

What does section 965 of the tax code mean?

In general, section 965 of the Code requires United States shareholders, as defined under section 951 (b) of the Code, to pay a transition tax on the untaxed foreign earnings of certain specified foreign corporations as if those earnings had been repatriated to the United States.

Who are specified foreign corporations under IRC section 965?

Foreign corporations with U.S. shareholders are called specified foreign corporations (SFC); this includes controlled foreign corporations (CFC) and any foreign corporation that has one or more domestic corporate shareholders. An important caveat to this decision is the fact that IRC section 965 (e) (2) expands CFC to include 10–50 corporations.

What is excluded from tested income under sec.951a?

Consistent with the definition of tested income under Sec. 951A (c) (2), the proposed regulations exclude from tested income any Subpart F income of a CFC that is excluded from foreign base company income or insurance income solely by reason of the high – tax exception.

When was section 956 added to the tax code?

Section 956 was first included with the introduction of Section 951 and Subpart F income as part of the Revenue Act of 1962. These foreign income tax reporting rules encapsulate US taxpayers that hold at least 10% of a Controlled Foreign Corporation, or CFC.