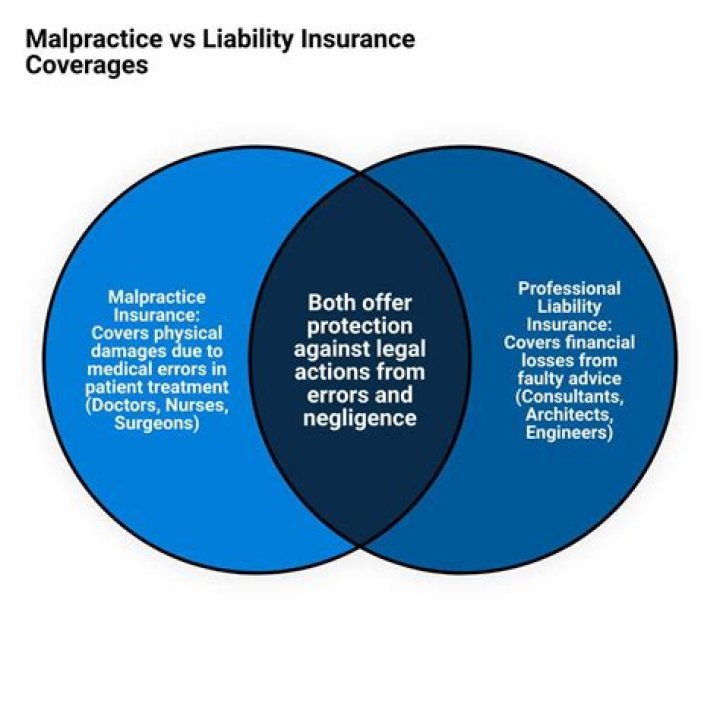

What is a tail coverage in malpractice insurance?

Tail malpractice coverage provides insurance coverage for claims brought after a claims-made insurance policy is terminated. This means there is no coverage for a claim brought after a claims-made policy is cancelled or not renewed. Tail malpractice coverage solves this problem.

How long do I need tail coverage?

“But I would advise them to take at least 5 years, because that gives you coverage for the basic statute of limitations in most states. Three-year tails do yield savings, but often they’re not enough to warrant the risk.” Another way to reduce costs is to lower the coverage limits of the tail.

How long does malpractice tail coverage last?

Most tail quotes are only good for 30-60 days and once the quote expires, you cannot have it reissued. It’s important that you plan ahead for the purchase of your tail insurance and begin considering outside finance options, if necessary.

Is prior acts coverage the same as tail coverage?

Claims made policies have distinct limitations on occurrences that happened before the policy’s inception (starting date), and after policy coverage ends. Prior acts are events that happened before a policy was in place, and “Tail” is the term for after the policy ends.

How is tail insurance calculated?

Tail insurance generally costs approximately 200% of the expiring claims-made premium. For example, let’s say your annual premium is $10,000. Then your tail coverage would cost around $20,000.

How much does tail coverage cost?

How much does tail coverage cost? Tail insurance generally costs approximately 200% of the expiring claims-made premium. For example, let’s say your annual premium is $10,000. Then your tail coverage would cost around $20,000.

How long do you need tail coverage?

How long should tail coverage last? While there are shorter tail options available, such as 2 or 3 three years, most tail coverage policies last a lifetime. Since malpractice claims can take years to be filed, we recommend physicians purchase lifetime tail coverage.

Tail insurance generally costs approximately 200% of the expiring claims-made premium. For example, let’s say your annual premium is $10,000. Then your tail coverage would cost around $20,000. While many doctors accept the first tail quote they are given, savvy doctors who work with MEDPLI save 20% on average.

How is tail coverage calculated?

How much does my tail cost? Tail calculation for a standard Medical Malpractice Insurance Policy: Answer: Ask your insurance Carrier for the last year’s non discounted annual premium. That is your basis for this calculus: multiply that basis x 2.0 or 2.5 (or somewhere in between); this will produce your tail premium.

What does tail mean in medical malpractice insurance?

Optional Extended Reporting Period Coverage, more commonly known as Malpractice Insurance Tail Coverage, is an insurance product purchased so that liability coverage extends beyond the end of the policy period of your claims-made medical malpractice insurance coverage.

How much does a tail insurance policy cost?

How much does tail coverage cost? A good rule of thumb for estimating the cost of tail coverage is to double the amount of the premium at the time of cancellation. The typical price ranges from 150-300% of the underlying premium, not including discounts.

Do you have to have tail insurance to be a doctor?

The coverage is optional and can be expensive, but it is highly recommended that physicians choose to purchase the endorsement to protect themselves from potential claims that may arise as a result of prior acts. It should be noted that most policies provide a free tail for retirement, death, or disability.

How does medical malpractice insurance policy work?

Most malpractice insurance policies are issued on a claims-made basis. With claims-made insurance, the policy will respond to claims made while the policy is in force, provided the services that caused the claim were rendered after the policy retroactive date.