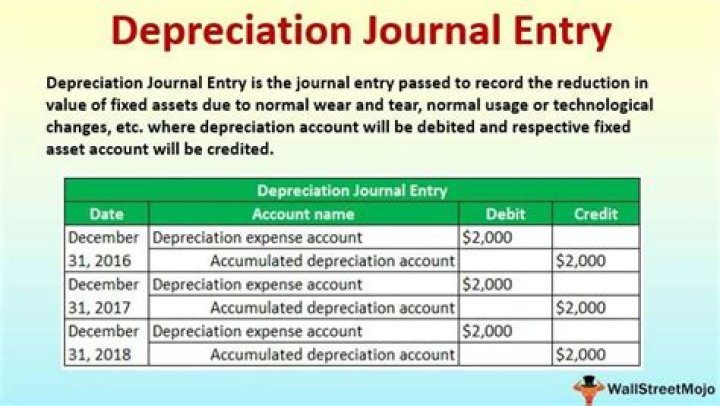

What is the entry to record depreciation?

The basic journal entry for depreciation is to debit the Depreciation Expense account (which appears in the income statement) and credit the Accumulated Depreciation account (which appears in the balance sheet as a contra account that reduces the amount of fixed assets).

When should depreciation first be recorded?

Depreciation of an asset begins when it is available for use, i.e. when it is in the location and condition necessary for it to be capable of operating in the manner intended by management.

Is depreciation recorded in the first year?

First, to establish account balances that are appropriate at the date of sale, depreciation is recorded for the period of use during the current year. Second, the amount received from the sale is recorded while the book value of the asset (both its cost and accumulated depreciation) is removed.

What happens when a company records depreciation?

Depreciation is an accounting process by which a company allocates an asset’s cost throughout its useful life. In other words, it records how the value of an asset declines over time. The purpose of recording depreciation as an expense is to spread the initial price of the asset over its useful life.

How do you record the depreciation?

Depreciation is recorded by debiting Depreciation Expense and crediting Accumulated Depreciation. This is recorded at the end of the period (usually, at the end of every month, quarter, or year). Depreciation Expense: An expense account; hence, it is presented in the income statement.

Do you charge depreciation in the year of purchase?

This is usually communicated by stating that a full year’s depreciation is charged in the year an asset is purchased, and no depreciation is charged in the year of its disposal. The alternative treatment is that depreciation is only charged for the part of the year for which an asset is held.

When do you record depreciation as an expense?

When a fixed asset is acquired by a company, it is recorded at cost (generally, cost is equal to the purchase price of the asset). This cost is recognized as an asset and not expense. Depreciation expense is recorded to allocate costs to the periods in which an asset is used.

How to calculate the first year of depreciation?

The first year depreciation calculation would be: To calculate depreciation by month: Your sum-of-the years depreciation calculation and expense will change each year, with each subsequent year using the declining number. For example, the calculation for the second year would be:

How to calculate straight line depreciation for a machine?

The straight line depreciation for the machine would be calculated as follows: 1 Cost of the asset: $100,000 2 Cost of the asset – Estimated salvage value: $100,000 – $20,000 = $80,000 total depreciable cost 3 Useful life of the asset: 5 years 4 Divide step (2) by step (3): $80,000 / 5 years = $16,000 annual depreciation amount

How is accumulated depreciation used in a business?

Depreciation expense is used to better reflect the expense and value of a long-term asset as it relates to the revenue it generates. Accumulated Depreciation Accumulated depreciation is the total amount of depreciation expense allocated to a specific asset since the asset was put into use.