What makes a trust eligible for Form 1041?

To put it simply, trusts and estates eligible for Form 1041 are: 1 Those that can report at least $600 in income or gains for that year. 2 As well as trusts and estates with one or more non-resident alien beneficiaries. More …

Do you have to file a 1041 tax return?

Normally, a trust must file Form 1041, U.S. Income Tax Return for Estates and Trusts, each calendar year. However, for most grantor trusts, filing Form 1041 is optional.

Do you have to file Form 1041 for QSST?

For a QSST, a Form 1041 must be filed each year. Also, regardless of the reporting method used (i.e., a Form 1041 or one of the alternative methods), the grantor tax information letter must be sent to each deemed owner.

How does a grantor trust file a Form 1099?

In this way, the Forms 1099 or Schedules K-1 would be issued in the grantor’s SSN, and the grantor’s name would be the first item in the name section, followed by a reference to the trust. This technique gives the trustee the option to avoid filing either an annual income tax return or Forms 1099.

Do you have to file a tax return for a special needs trust?

If the SNT’s income must be reported by the beneficiary on his own personal return, the SNT document should allow the SNT to pay the beneficiary’s income tax liability from the assets in the SNT.

What kind of trust is a special needs trust?

Third-party SNTs are generally considered either “complex trusts” or “qualified disability trusts” for income tax purposes. The SNT itself is responsible for reporting its own items of income, deduction and credit.

Do you have to file a Form 1041 with the IRS?

You may file for an extension of time to file, using a Form 7004. Not all estates and trusts must file IRS Form 1041. Yet, unlike the name suggests, there are trusts that must file a Form 1041 even if they don’t have any income for the tax year.

Who is required to file a 1041 tax return?

The fiduciary of a domestic decedent’s estate, trust, or bankruptcy estate files Form 1041 to report: The income, deductions, gains, losses, etc. of the estate or trust.

When to report excess deductions on Form 1041?

Schedule K-1 (Form 1041) Instructions—Corrected Decedent’s Schedule K-1– 29-JAN-2021 Reporting Excess Deductions on Termination of an Estate or Trust on Forms 1040, 1040-SR, and 1040-NR for Tax Year 2018 and Tax Year 2019 —

When do estates and trusts do not need to file tax returns?

For Estates With No Income. If the estate or trust has no income, or a gross income of less than $600 within the tax year, then there is no need to file a return. However, if one of the beneficiaries is a nonresident alien, then a trust or estate must file a tax return (even if it does not have any income). Deductions for Estates and Trusts

When do I need to send Form 1041 to MEF?

In Processing Year 2021, MeF will accept Form 1041 Tax Years 2018, 2019, and 2020. In addition to prior tax years, MeF offers the ability to: File amended 1041 returns Attach any supporting documents as a PDF (Note: Documents can no longer be mailed to IRS if Form 1041 is filed electronically)

What is the e-file for estates and trusts?

e-file for Estates and Trusts Form 1041, U.S. Income Tax Return for Estates and Trusts, is used by the fiduciary of a domestic decedent’s estate, trust, or bankruptcy estate to report: Estates and Trusts | Internal Revenue Service Skip to main content An official website of the United States Government English Español 中文 (简体) 中文 (繁體)

How many tax returns are filed for trusts and estates?

This is not surprising because of the comparatively few taxpayers affected. In the 2008 tax year, approximately 3 million Forms 1041, U.S. Income Tax Return for Estates and Trusts, were filed, with an aggregate gross income of $188 billion.

How is the taxable income of a Trust calculated?

The estate’s or trust’s taxable income is computed using the following formula: Gross income Less Deductible trust expenses Less Personal exemption amount Equals Taxable income before distribution dedu Less Distribution deduction

When do you have to file a 1041 tax return?

Form 1041. Trustees must file Form 1041 if any filing requirement is triggered, even if the trust owes no taxes. Form 1041 reports trust income, deductions and capital gains and losses.

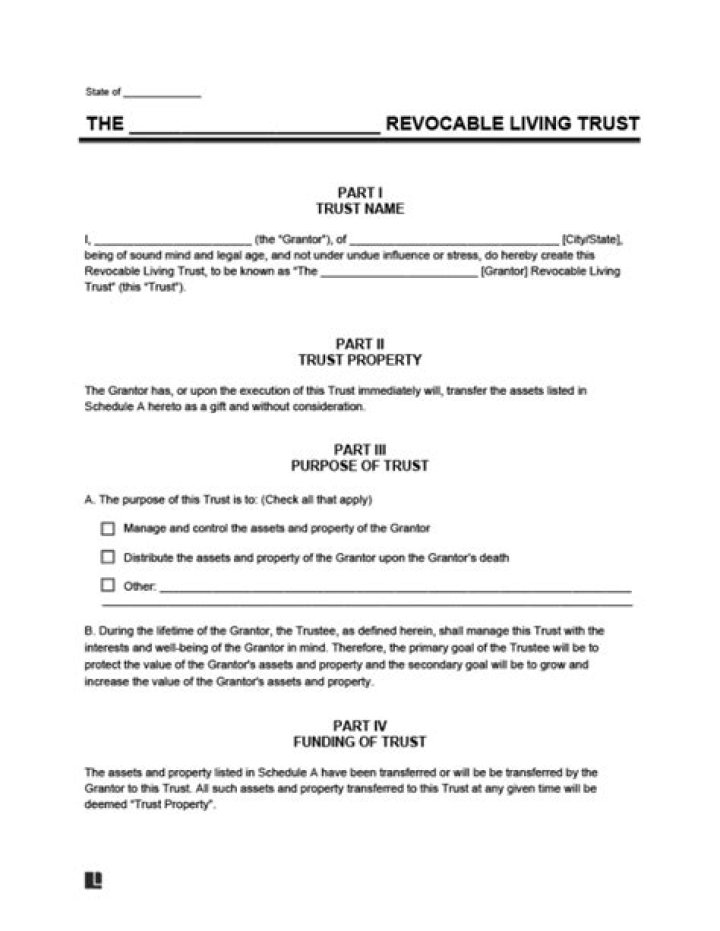

What kind of tax return do I need for an irrevocable trust?

An irrevocable trust uses form 1041 unless it is declaring charitable donations in which case it must file IRS form 1041A – U.S. Information Return Trust Accumulation of Charitable Amounts. The trustee is generally required to sign the 1041 or 1041A.

How to create an irrevocable family trust agreement?

In order to create an irrevocable family trust agreement, the person or people creating the trust (the grantors or settlors) must enter into a written, legal agreement with the person or organization that will manage trust assets (the trustee).

When do estates have to file Form 1041?

For fiscal year estates and trusts, file Form 1041 by the 15th day of the 4th month following the close of the tax year.

Do you have to pay taxes on a 1041 form?

Form 1041 for simple estate says taxes are due. Can the estate pay the tax if the income has not been distributed, avoiding K-1 to beneficiaries? Yes, but you have to understand that a distribution will carry out DNI (distributable net income).

When to file a 1041 for an estate?

Complex or Simple depending upon the trust instrument (refer to the information in the link below). A separate 1041 for the estate does not need to be filed unless the estate has $600 or more in gross income, which would be virtually impossible if the estate has no income-producing assets. September 14, 2019 2:40 PM

Who is a skip beneficiary on Form 1041?

Question 9 is looking for information about skip beneficiaries so that the IRS can attempt to collect even more tax under the generation-skipping transfer tax rules. Generally, a skip beneficiary is someone who’s more than one generation below that of the transferor of the property.

When to file TD F 90-22.1 for a trust?

If you answer “yes” and the combined total of all foreign accounts is greater than $10,000, you may have to file Form TD F 90-22.1, Report of Foreign Bank and Financial Accounts. If the trust or estate has no foreign accounts but owns foreign securities in a U.S.-based account, the answer to this question is “no.”