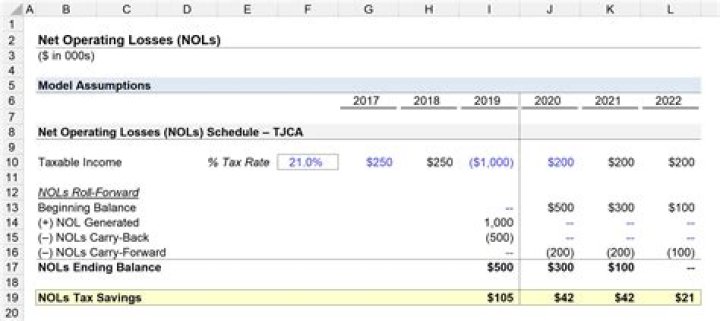

When is section 382 limitation on net operating loss increased?

the long-term tax -exempt rate. If the section 382 limitation for any post-change year exceeds the taxable income of the new loss corporation for such year which was offset by pre-change losses, the section 382 limitation for the next post-change year shall be increased by the amount of such excess.

What is the carryforward of the section 382 limitation?

(2) Carryforward of unused limitation. If the section 382 limitation for any post-change year exceeds the taxable income of the new loss corporation for such year which was offset by pre-change losses, the section 382 limitation for the next post-change year shall be increased by the amount of such excess.

What are the rules for limitation under section 383?

Similar rules shall apply in the case of any credit or loss subject to limitation under section 383. taxable income shall be treated as having been offset first by the loss subject to such limitation. in the case of attribution from another entity, an interest in such entity similar to stock described in subclause (I).

Are there any misconceptions about student loan debt?

There are nearly as many misconceptions about student loan debt as there are ways to obtain and pay for it. Too often, college students rely on peers for advice on rules on responsibilities. In the process, a lot of half-truths or just plain misinformation is passed along. Some of the more popular misconceptions regarding student loans include:

How is long term capital loss treated in S corporation?

A then reduces stock basis to zero for $2,000 of the $7,000 long-term capital loss. Assuming A has no basis in S Co.’s indebtedness, the remaining $5,000 of long-term capital loss must be carried forward, where it will be treated as a newly incurred loss in 2014.

When does the net operating loss of an old loss Corporation?

the net operating loss of the old loss corporation for the taxable year in which the ownership change occurs to the extent such loss is allocable to the period in such year on or before the change date.

When is a recognized built-in loss treated as a deduction?

Any amount which is allowable as a deduction during the recognition period (determined without regard to any carryover) but which is attributable to periods before the change date shall be treated as a recognized built-in loss for the taxable year for which it is allowable as a deduction.